3PL Market Roundup – Q1 2025: Warehouse Storage Rates

A review of 3PL storage rates in Q1 2025 around Australia

Welcome to uTenant’s 3PL Market Roundup report for Q1 CY2025. This report looks at ambient pallet storage rates across Australia from January to March (inclusive); providing valuable insights for businesses seeking third-party logistics (3PL) warehousing solutions, whilst also allowing 3PL providers to benchmark their own rates. We leverage data from our Warehouse Storage and 3PL (PalletMatch) service to present median storage rates for each State and give you an indication of the current 3PL landscape.

Overall, the national median pallet storage rate increased by about 13% compared to the previous quarter. There are many factors in the mix that have likely contributed to this:

- Rising operating costs

- Warehouses holding more stock post-December because retail sales fell short of forecasts, and then back-to-school and Easter stock has added to inventory holdings

- Correction of rates back to “normal” after heavy discounting in Q4 2024

The late-2024 softening in storage rates provided a window for renegotiating warehouse contracts or securing additional space at better prices. Those who took advantage may lock in cost savings. But companies must also plan for potential increases in storage demand and costs later in 2025 if consumption accelerates or if currently “loose” markets tighten again.

Macroeconomic conditions in Q1 2025

Across Australia’s states, economic conditions varied slightly but all faced the broad national trends of high costs and soft demand. Resource-rich states like Western Australia (WA) benefited from a late-2024 rebound in commodity exports (e.g. minerals and energy), thanks to improving global demand – exports of goods rose toward the end of 2024. However, States dependent on household spending (like Victoria (VIC) and New South Wales (NSW)) saw consumers tightening belts under cost-of-living pressures and interest burdens.

No State was immune to the economic slowdown, but those with exposure to exports or tourism (e.g. Queensland (QLD) with revived tourism, and WA with commodities) had pockets of resilience, whereas States focused on domestic consumption felt the squeeze of cautious spending. These State-level dynamics also played into warehousing demand and storage pricing, as discussed later.

In the RBA’s most recent Statement on Monetary Policy (February 2025), the RBA noted the outlook for inflation, unemployment and economic growth remains uncertain, with recent data giving mixed signals about the state of the economy. On the global front, new trade policies could lead to slower growth and potentially higher inflation for some countries.

Australia’s industrial and logistics real estate market has been exceptionally tight in recent years, though signs of normalisation began emerging by late 2024. After record-low warehouse vacancy rates in 2022–2023 (driven by the e-commerce boom and supply chain disruptions), new supply delivery and tempered demand started to ease the pressure.

By the second half of 2024, the national average warehouse vacancy rate had inched up to about 2.5% (from historic lows nearer 1% a year prior). This 2.5% vacancy is still extremely low in global terms, underscoring that Australia’s warehouse space remains scarce and valuable, however, the upward tick in vacancy indicates that new warehouses coming online are not being absorbed as quickly as before.

Developers delivered a substantial amount of new logistics space in 2024, and a similar supply pipeline is slated for 2025. With roughly 40% of this new industrial space pre-leased, and the remaining 60% speculative space, it’s likely to put upward pressure on vacancy rates in 2025, giving tenants more options. Indeed, industrial landlords have increasingly had to offer incentives(such as rent-free periods or fit-out contributions) to secure tenants, which has slowed the growth of effectiverents even where face rents remain high.

3PL storage rates in Q1 2025 around the country

The data presented in this report is based on uTenant's internal data set, gathered through our PalletMatch service (undertaken with our National network of 3PL providers and customers), and may not be fully representative of the entire Australian 3PL market. It’s important to note that, pallet storage rates can vary widely based on factors such as location, warehouse size, services provided, duration of storage, and the specific business industries we're working with.

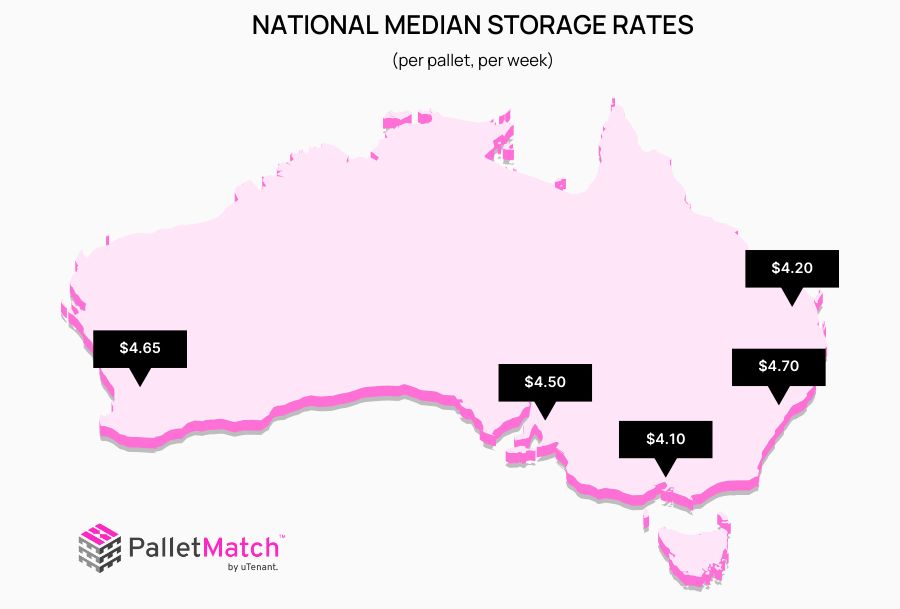

The National median storage rate for Q1 2025 is $4.50 pppw1, up from $4.00 pppw1 reported in Q4.

This quarter, NSW had the greatest variation in storage rates with a low of $3.00 pppw1 and a high of $7.00 pppw1, but ambient pallet storage rates in WA saw the most dramatic spike with a new high of $7.00 pppw1. QLD’s range of $3.15 pppw1 to $5.00 pppw1 remained fairly stable; as did VIC with a range of $3.00 pppw1 to $4.25 pppw1, and SA shifted slightly upward with a range of $3.00ppw1 to $5.00 pppw1.

Each quarter, uTenant's network of 3PL providers share their pallet storage rates with the PalletMatch team; enabling us to produce this insightful industry report for 3PL providers and product owners alike.

The 3PL landscape, Q1 2025

This quarter we’ve seen rates returning to normal levels, after the modest decline in ambient pallet storage rates we saw from 3PL providers last quarter. As we noted in our Q4 2024 3PL Market Roundup, the drop in rates in Q4 was likely due to a shift in demand patterns and increase competition amongst 3PL providers. Many 3PL providers were under pressure to keep prices competitive as their customers sought to cut logistics costs. It truly became a buyer’s market for storage toward the end of 2024 in many regions.

Looking ahead from Q4 2024 into Q1 2025, there are several factors likely to shape ambient storage pricing:

- Seasonal demand spikes: Back-to-school and Easter were expected to temporarily firm up rates in early 2025 as warehouses handle increased turnover. This indeed caused short-lived tightening in specific sub-sectors.

- Regional infrastructure investments: Continued investment in logistics infrastructure (e.g. inland freight terminals, highway upgrades in regional areas) could bring more affordable warehousing options online in regional towns, slightly expanding the geography of available storage and relieving metro capacity.

- Global supply chain shifts: Many companies are still reconfiguring supply chains post-pandemic – for example, diversifying sourcing away from single countries, thereby easing volatility in storage demand. A more stable global supply chain means fewer shock spikes in Australian warehouse needs, however, this is likely to be shaken by recent announcement of global tariffs by the United States.

- China’s economic trajectory: An economic stimulus program in China and improved China-Australia trade activity could increase the flow of goods through Australian ports, raising demand for 3PL services and potentially pushing pallet storage rates higher if imports/exports accelerate. (China is Australia’s largest trading partner, so an uptick in Chinese demand can boost volumes of commodities and consumer goods moving through Australian warehouses.)

- Inflation and cost dynamics: With inflation now low, any re-acceleration (for instance, if global commodity prices rise) could quickly translate into higher operating costs for warehouses (fuel, electricity, wages). 3PL providers signaled that if their costs start climbing again in 2025, they will seek to adjust storage pricing upward accordingly. Conversely, if economic weakness persists and demand stays soft, providers may hold or even cut rates to stay competitive.

In summary, the ambient warehousing market in early 2025 is dynamic and at an inflection point. After 2024, where demand fell short of expectations and new industrial property capacity came online, the 3PL market is starting to normalise (for now). The announcement of tariffs between the United States and other major economies poses challenges to the global outlook. But the scale and incidence of the tariffs and their effects remain highly uncertain.

Structural factors (ongoing high input costs, historically low vacancy, and a potential rebound in activity) suggest any softening in the 3PL landscape will only be temporary. Businesses planning their logistics budgets in 2025 would do well to lock in favourable storage contracts now, while also building in flexibility for possible rate adjustments later in the year if conditions tighten again.

In every State, except New South Wales, we have seen an increase in rates back (or close) to Q3 2024 levels. There are still opportunities for businesses to secure reasonable storage rates with 3PL providers though, if you look in the right place (hint: that’s uTenant’s network of vetted 3PL providers).

Many experts are predicting multiple rate cuts in 2025, which should help with growth and spending. If this plays out, we should see a “return to normality” in pallet storage rates, however, operational costs, property, the labour market and demand will continue to play big roles in influencing pallet storage rates in each State in 2025.

3PL landscape insights, Q1 2025

Recommendations for businesses

- Benchmark your costs: Use the rates in this report to compare your current storage rate agreements. If you’re paying significantly above the average, consider renegotiating terms or exploring alternative 3PL providers.

- Enhance forecasting accuracy: With rates influenced by macroeconomic factors, improving inventory forecasting can help mitigate over-reliance on expensive storage.

- Explore value-added services: Assess whether your 3PL provider offers complementary services that can offset storage costs, such as cross-docking or fulfillment services.

- Invest in technology: Utilise warehouse management systems (WMS) to gain visibility into your storage needs and identify opportunities to consolidate inventory.

Domestically, high input costs and labor shortages in warehousing are still unresolved issues; if anything, the industry’s 2024 experience of margin squeeze may drive some smaller 3PL operators out of the market or discourage new warehouse construction beyond the current pipeline. This could set the stage for a tighter market in the medium term. As we noted in our last report, the RBA’s uncertainty on the economic outlook will fuel uncertainty in the 3PL market, leading to highly varied storage rates and strategies across regions.

By staying informed and being proactive, businesses can better navigate the dynamic 3PL landscape. With the support of uTenant, businesses can benchmark and secure the best warehousing solutions for their needs, whether that be better 3PL storage rates or sharper rent if leasing your own warehouse.

Additional considerations

Beyond the headline rates, several other factors can influence the final cost of ambient pallet storage and should be taken into consideration:

- Warehouse features: Warehouses with advanced features like state-of-the-art security systems, temperature control, automation, or environmental sustainability credentials will naturally command higher rates compared to basic storage facilities.

- Contract terms: The length and structure of your contract with a 3PL provider can significantly impact the final cost per pallet. Negotiating longer contracts or committing to minimum storage volumes may lead to lower per-unit rates.

- Location: Prime locations in major cities will typically have higher 3PL storage rates than regional areas. Businesses should consider their specific needs and distribution requirements when determining the optimal warehouse location.

Q1 2025 - The 3PL market remains dynamic

As 2025 progresses, the ambient pallet storage market is expected to remain dynamic – influenced by macroeconomic recovery (or lack thereof) and the aftershocks of global events, most notable the recent U.S. tariff impacts. 3PL providers and warehouse operators will need to remain vigilant, adaptable, and strategic in managing their supply chain real estate, whilst businesses relying on 3PL services should keep a close on rates and service levels to ensure they’re in a mutually beneficial partnership.

The 3PL Market Roundup report is published on a quarterly basis, in the month following the end of the calendar quarter. See 3PL Market Roundup - The methodology behind the numbers, for a deeper explanation of the report and its purpose.

It's important to note that the pallet storage figures in this report are based on uTenant’s network of 3PL providers and will change over time. To get accurate and current pricing information, we recommend contacting us directly to discuss your specific 3PL and warehouse storage needs.

- uTenant PalletMatch Team

uTenant’s team of experts have extensive knowledge of and experience in supply chain and logistics operations. With its vast 3PL provider network, uTenant is able to match clients with warehouse space specific to their current or growing needs. To put it simply, uTenant's purpose-built PalletMatch platform matches those looking for warehouse space, with those who have it – across Australia and New Zealand. Find out more about Pallet Matching and how it can help you.

If you have warehouse space to fill, get in touch with the uTenant team now.

If you are looking for warehouse space click the button below to start your search with uTenant.

1Benchmarked on per pallet per week (pppw) or part thereof.

Published: 29 April 2025